Fighting Britain's £50bn Late Payments Crisis

In a market where SMEs were spending 1.5 hours daily chasing payments that arrived 23 days late, we believed financial technology could fix what broken processes couldn't.

SME Customers

SME customers onboarded across diverse UK business sectors

Investment Raised

Strategic investment from Lakestar & Six Fintech (UBS/Credit Suisse)

Revenue Increase

Increase in revenue per customer through debt recovery and BNPL products

"In a market where SMEs were spending 1.5 hours daily chasing payments that arrived 23 days late, we believed financial technology could fix what broken processes couldn't.

"

The Brief

Businesses were spending more time chasing money than making it

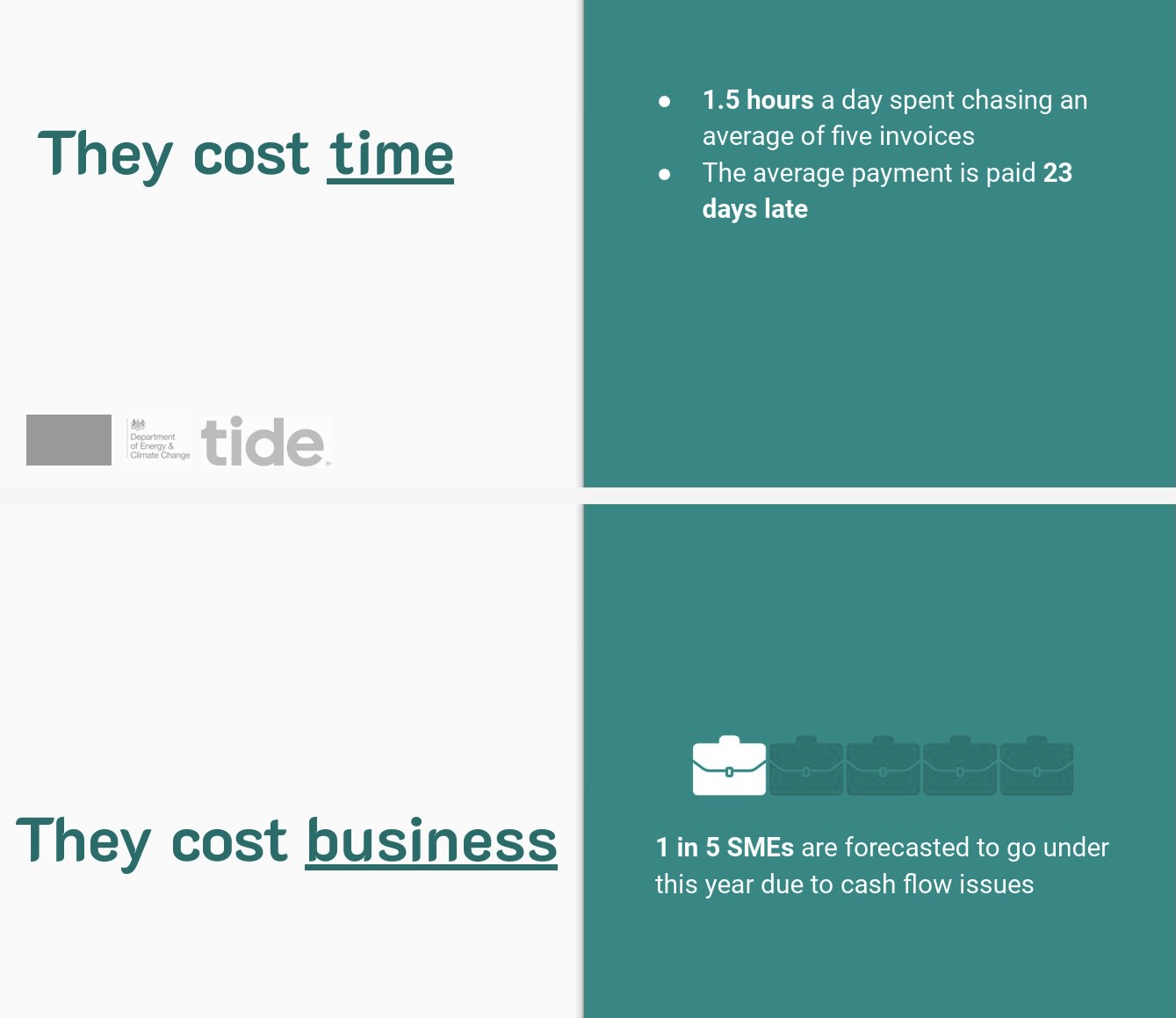

The numbers were staggering, hidden in plain sight across Britain's business landscape. £50 billion worth of late payments were being chased at any one time. Small and medium enterprises were spending £4.4 billion annually just pursuing money they were already owed. The average amount outstanding per business? £8,500 – enough to fund a new hire or critical equipment upgrade.

Behind these statistics lay a human cost that traditional finance rarely acknowledged. Business owners were dedicating 1.5 hours every single day to chasing an average of five overdue invoices. Payments that should have arrived on time were consistently landing 23 days late, creating a cascade of cash flow problems that rippled through entire supply chains. When small businesses couldn't pay their suppliers because they hadn't been paid themselves, the whole economic ecosystem began to fracture.

"Every late payment ripples through the economy. When small businesses can't pay suppliers because they haven't been paid, the whole system starts to break down."

The technology landscape in 2020 offered a tantalising glimpse of what might be possible. Open banking regulations were newly in place, creating rails for instant, secure, bank-to-bank transfers. Yet adoption among SMEs remained stubbornly low at just 10%. Most businesses were still trapped in manual processes – typing bank details, waiting days for transfers to clear, drowning in administrative overhead that consumed time better spent growing their companies.

Existing solutions felt like sticking plasters on a broken system. Stripe demanded substantial fees and exposed businesses to chargebacks. PayPal imposed high charges, frequent payment freezes, and forced companies to fund and withdraw money via cards or bank accounts. Pingit, despite Barclays' backing, offered a clunky process limited to single bank accounts and wasn't built on open banking infrastructure. None addressed the fundamental problem: business payments were still designed for a world that no longer existed.

The founding conviction emerged from this frustration. With Darren and my deep experience building Crowdcube into Britain's largest equity crowdfunding platform and Pete's product expertise from the fintech trenches, there was a shared belief that business payments could be as seamless as consumer banking had become. The question wasn't whether the technology existed – it was whether anyone had the determination to build it properly.

Liz Barclay was right behind our mission

The smaller the business the less likely to be paid on time

Late payments is an existential risk for small businesses

The Brief

Businesses were spending more time chasing money than making it

Liz Barclay was right behind our mission

The smaller the business the less likely to be paid on time

Late payments is an existential risk for small businesses

The numbers were staggering, hidden in plain sight across Britain's business landscape. £50 billion worth of late payments were being chased at any one time. Small and medium enterprises were spending £4.4 billion annually just pursuing money they were already owed. The average amount outstanding per business? £8,500 – enough to fund a new hire or critical equipment upgrade.

Behind these statistics lay a human cost that traditional finance rarely acknowledged. Business owners were dedicating 1.5 hours every single day to chasing an average of five overdue invoices. Payments that should have arrived on time were consistently landing 23 days late, creating a cascade of cash flow problems that rippled through entire supply chains. When small businesses couldn't pay their suppliers because they hadn't been paid themselves, the whole economic ecosystem began to fracture.

"Every late payment ripples through the economy. When small businesses can't pay suppliers because they haven't been paid, the whole system starts to break down."

The technology landscape in 2020 offered a tantalising glimpse of what might be possible. Open banking regulations were newly in place, creating rails for instant, secure, bank-to-bank transfers. Yet adoption among SMEs remained stubbornly low at just 10%. Most businesses were still trapped in manual processes – typing bank details, waiting days for transfers to clear, drowning in administrative overhead that consumed time better spent growing their companies.

Existing solutions felt like sticking plasters on a broken system. Stripe demanded substantial fees and exposed businesses to chargebacks. PayPal imposed high charges, frequent payment freezes, and forced companies to fund and withdraw money via cards or bank accounts. Pingit, despite Barclays' backing, offered a clunky process limited to single bank accounts and wasn't built on open banking infrastructure. None addressed the fundamental problem: business payments were still designed for a world that no longer existed.

The founding conviction emerged from this frustration. With Darren and my deep experience building Crowdcube into Britain's largest equity crowdfunding platform and Pete's product expertise from the fintech trenches, there was a shared belief that business payments could be as seamless as consumer banking had become. The question wasn't whether the technology existed – it was whether anyone had the determination to build it properly.

The Approach

Technology as the great equaliser

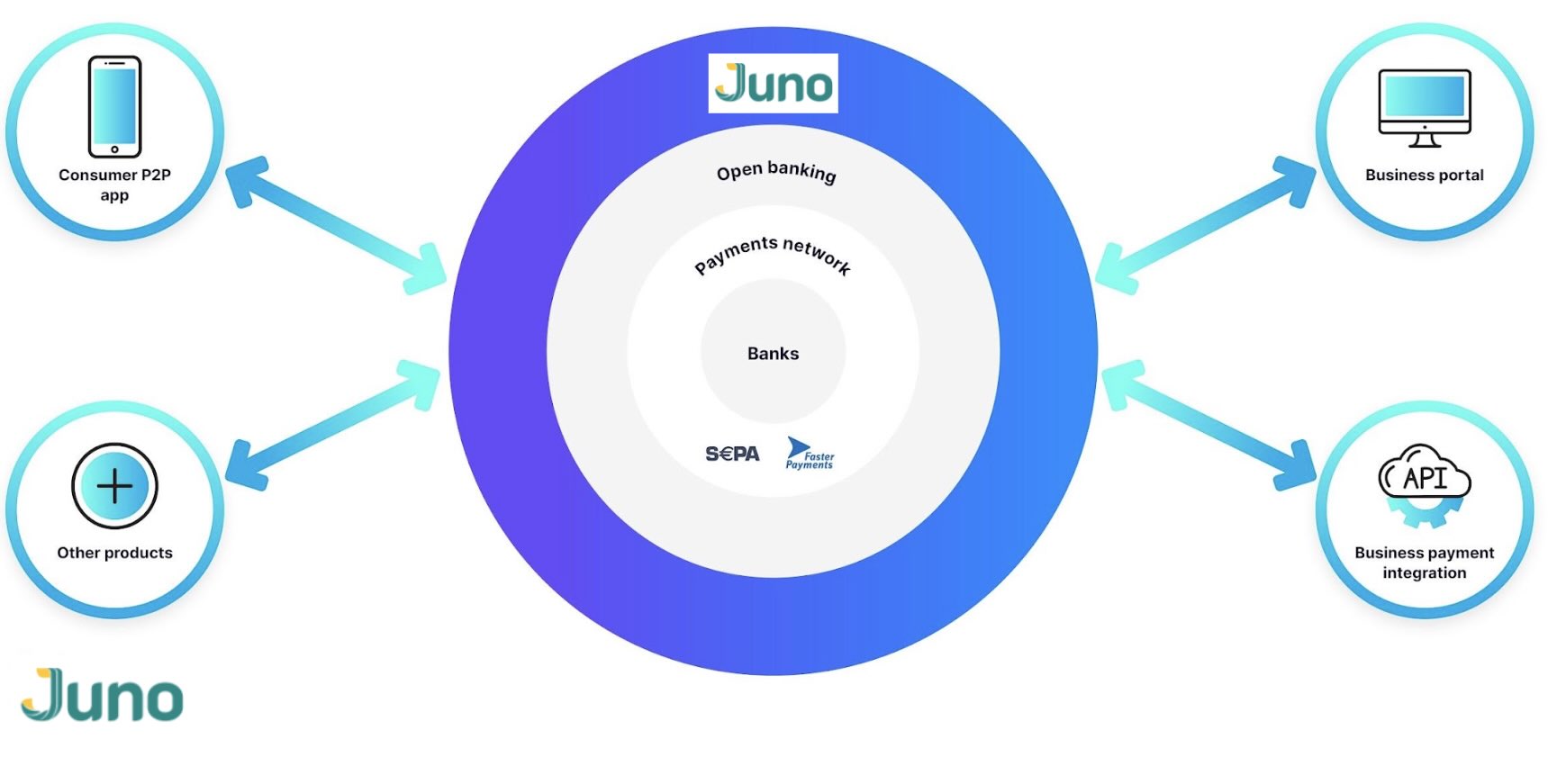

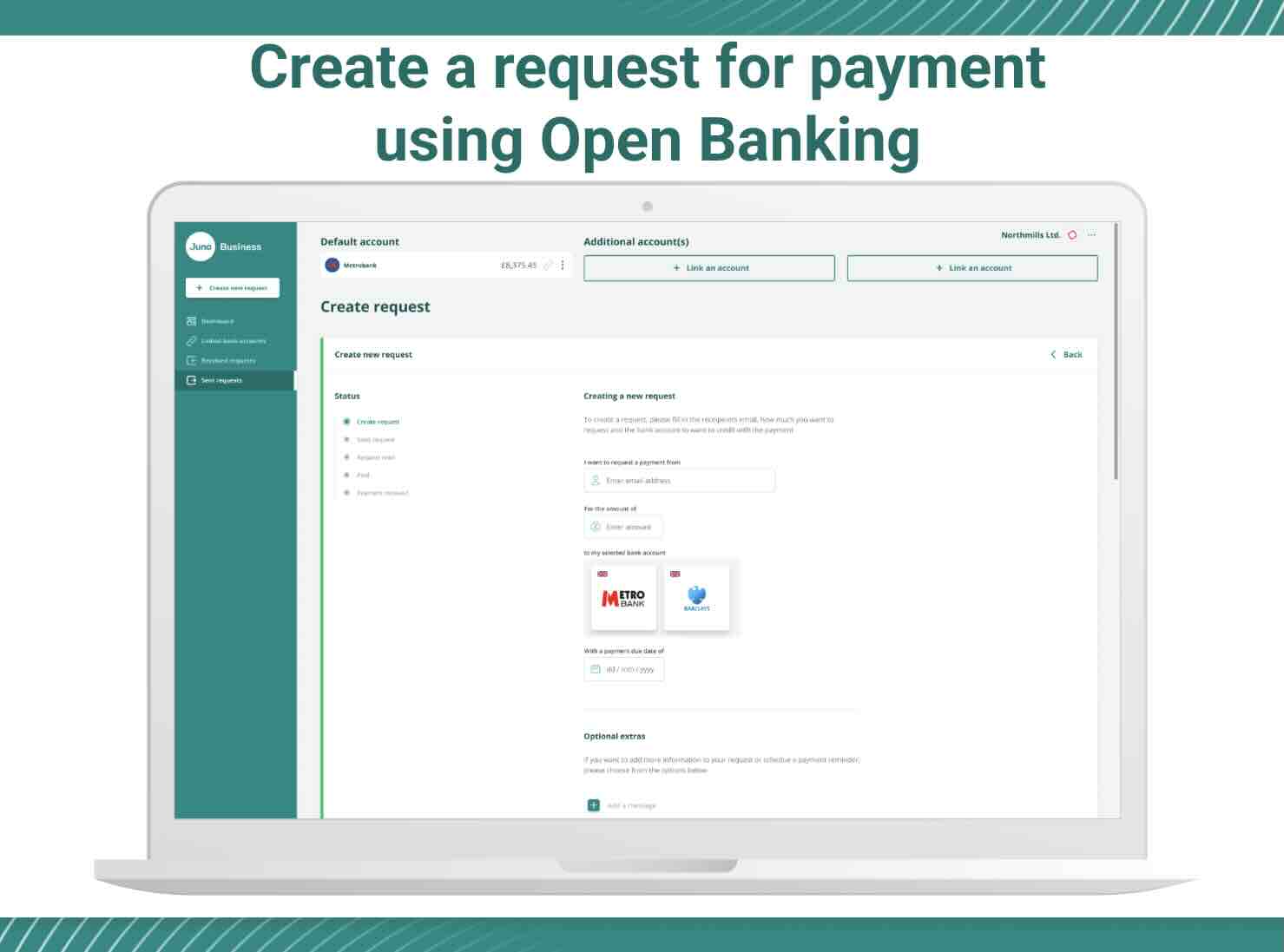

Open banking provided the foundation for everything that followed. Direct bank-to-bank transfers would eliminate the card fees that were bleeding SMEs dry, remove the chargeback risks that created accounting nightmares, and provide instant settlement that transformed cash flow management from reactive firefighting to proactive planning. The infrastructure was there; it just needed to be packaged in a way that made sense to time-pressed business owners.

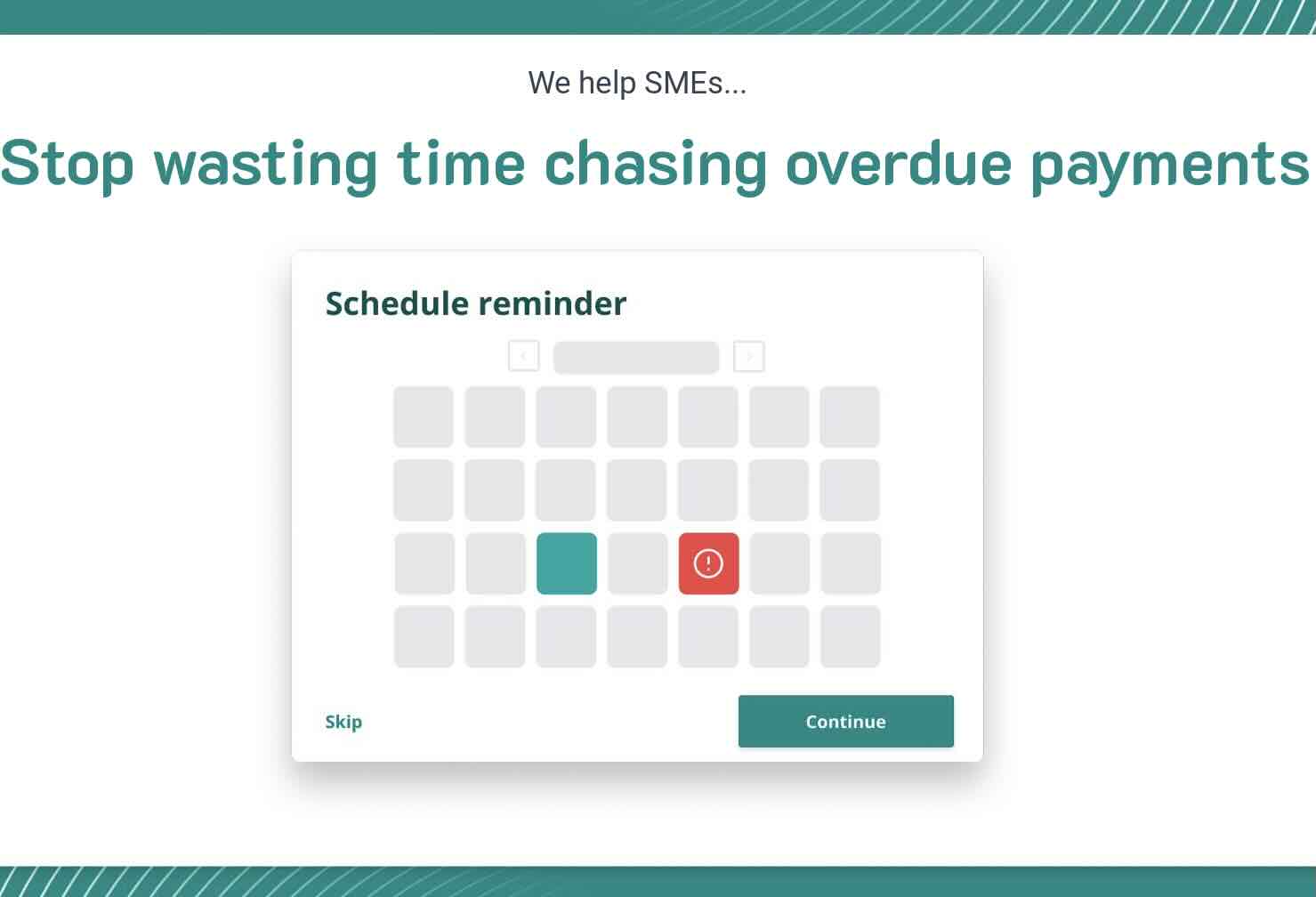

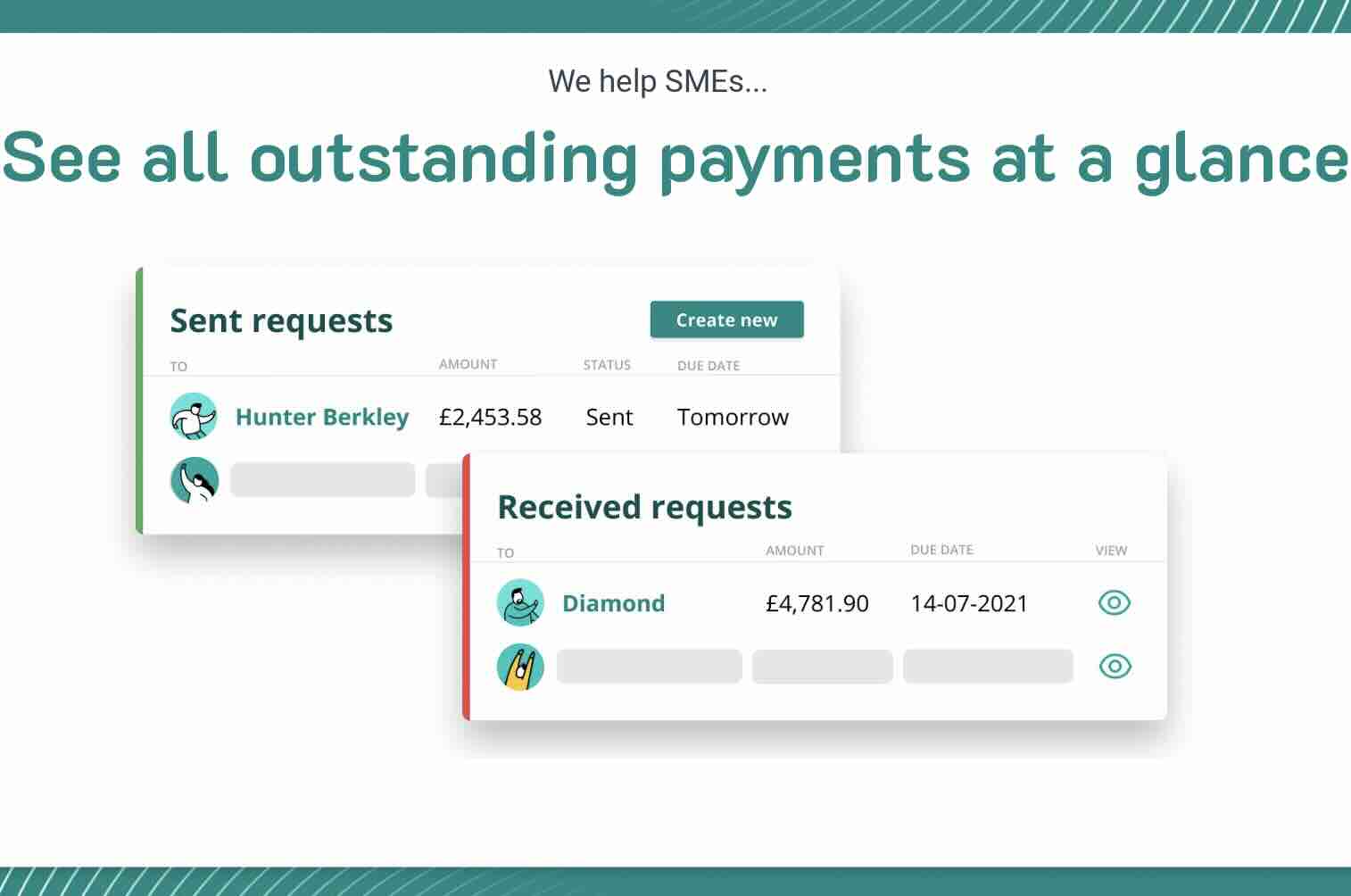

Automation became the core philosophy driving every product decision. If businesses were wasting hours daily chasing payments, then the solution was to build systems that made chasing obsolete. Smart dashboards would provide real-time cash flow visibility, showing not just what money was coming in, but when it would arrive and how it would impact the business. Payment requests would track themselves, send automatic reminders, and update status in real-time. The goal was simple: businesses should never have to chase a payment again.

Open banking had given us the rails. Our job was to build the trains that would actually get businesses where they needed to go.

The competitive landscape revealed exactly where the opportunity lay. Against Stripe's escalating fees, we could offer free or very low-cost transactions. Against PayPal's fraud risks and payment freezes, we could provide bank-level security with transparent processes. Against Pingit's single-bank limitations, we could deliver multi-bank support with European coverage from day one. The incumbent solutions were designed for a different era – we were building for the world that was emerging.

Strategic partnerships became the credibility anchor for everything else. Targeting FCA authorisation signalled serious intent to regulators and customers alike. Building relationships with Barclays opened doors to established business networks. Connecting with Binance demonstrated our understanding of digital finance evolution. Partnering with the Federation of Small Businesses provided direct access to the pain points we were trying to solve. Each relationship added legitimacy to a mission that required businesses to trust us with their financial futures.

The product philosophy emerged from first principles thinking about how business payments should work. API-first architecture ensured seamless integration with existing accounting systems and business tools. Mobile-first design acknowledged that business owners needed to manage cash flow on the go, not just from desktop computers. European coverage recognised that modern SMEs operated across borders from day one. Every technical decision was filtered through a simple question: does this make it easier for businesses to get paid?

Our survey alongside YouGov of 10,000 UK SMEs showed a desperate situation

Juno was originally BillX before a rebrand and focus on SME customers

Darren (Crowdcube Founder) and Charles (Comply Advantage Founder) were invaluable assets

The Approach

Technology as the great equaliser

Our survey alongside YouGov of 10,000 UK SMEs showed a desperate situation

Juno was originally BillX before a rebrand and focus on SME customers

Darren (Crowdcube Founder) and Charles (Comply Advantage Founder) were invaluable assets

Open banking provided the foundation for everything that followed. Direct bank-to-bank transfers would eliminate the card fees that were bleeding SMEs dry, remove the chargeback risks that created accounting nightmares, and provide instant settlement that transformed cash flow management from reactive firefighting to proactive planning. The infrastructure was there; it just needed to be packaged in a way that made sense to time-pressed business owners.

Automation became the core philosophy driving every product decision. If businesses were wasting hours daily chasing payments, then the solution was to build systems that made chasing obsolete. Smart dashboards would provide real-time cash flow visibility, showing not just what money was coming in, but when it would arrive and how it would impact the business. Payment requests would track themselves, send automatic reminders, and update status in real-time. The goal was simple: businesses should never have to chase a payment again.

Open banking had given us the rails. Our job was to build the trains that would actually get businesses where they needed to go.

The competitive landscape revealed exactly where the opportunity lay. Against Stripe's escalating fees, we could offer free or very low-cost transactions. Against PayPal's fraud risks and payment freezes, we could provide bank-level security with transparent processes. Against Pingit's single-bank limitations, we could deliver multi-bank support with European coverage from day one. The incumbent solutions were designed for a different era – we were building for the world that was emerging.

Strategic partnerships became the credibility anchor for everything else. Targeting FCA authorisation signalled serious intent to regulators and customers alike. Building relationships with Barclays opened doors to established business networks. Connecting with Binance demonstrated our understanding of digital finance evolution. Partnering with the Federation of Small Businesses provided direct access to the pain points we were trying to solve. Each relationship added legitimacy to a mission that required businesses to trust us with their financial futures.

The product philosophy emerged from first principles thinking about how business payments should work. API-first architecture ensured seamless integration with existing accounting systems and business tools. Mobile-first design acknowledged that business owners needed to manage cash flow on the go, not just from desktop computers. European coverage recognised that modern SMEs operated across borders from day one. Every technical decision was filtered through a simple question: does this make it easier for businesses to get paid?

The Breakthrough

The moments that made it feel possible

Investment validation arrived in the form of £1.6 million from Lakestar and Six Fintech – venture capital firms that understood both the fintech landscape and the specific pain points plaguing SMEs. These weren't just cheques; they were stamps of approval from investors who had seen countless payment solutions fail to gain traction. Their backing suggested that our approach to the problem was fundamentally sound, even if the execution remained to be proven.

The regulatory milestone came faster than anyone predicted. Achieving FCA authorisation for Account Information Services and Payment Initiation Services in just three months demonstrated that our compliance approach was robust and our team understood the complexities of financial regulation. While other startups struggled with regulatory hurdles for years, we had built the right foundations from the beginning. The authorisation wasn't just a legal requirement – it was proof that we could operate at the standards required to handle other people's money.

"The first time a customer told us they'd cancelled their debt collection service because they didn't need it anymore, we knew we'd found something real."

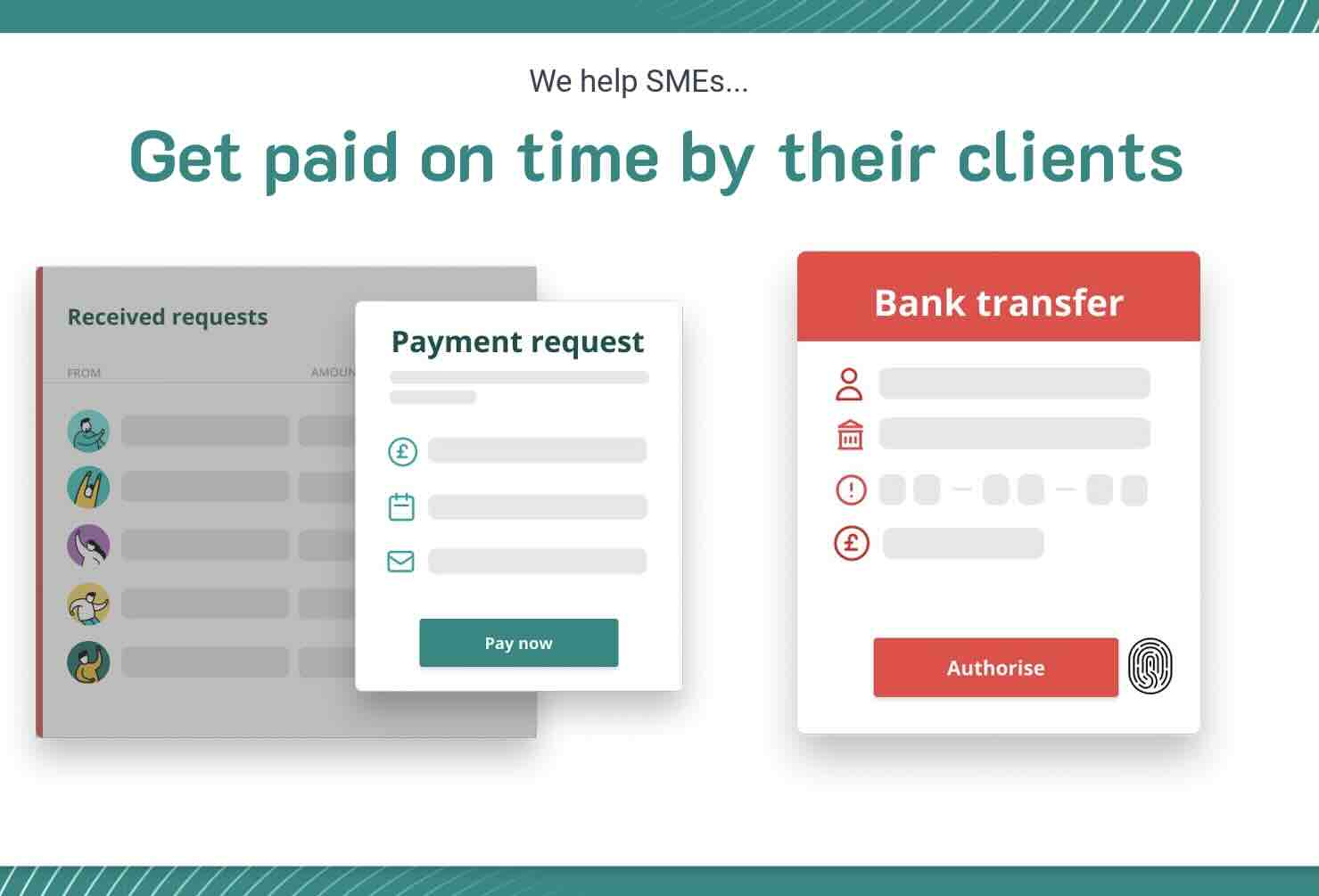

First customer wins validated every assumption about product-market fit. Businesses immediately embraced features that seemed obvious in hindsight but had never been available before. Payment URLs that could be copied and sent via email, WhatsApp, or any communication channel eliminated the friction of platform lock-in. Real-time cash flow dashboards gave business owners what Tom Whittle called "brilliant" visibility into their financial position. The automation meant companies could focus on serving customers instead of chasing payments.

The technology proved itself under real-world conditions that no amount of testing could replicate. Successfully integrating with all major UK banks despite the early instability of open banking infrastructure required constant troubleshooting and adaptation. When payment requests consistently completed successfully and money arrived in business accounts as promised, the platform demonstrated the reliability that cash-strapped SMEs desperately needed. Technical excellence became the foundation for customer trust.

Market feedback confirmed that we had identified something genuinely transformative. Customers consistently described Juno as "cheaper and faster than other payment alternatives we've used like GoCardless or PayPal." Amanda Baker noted that "every penny counts for small business owners like me." The testimonials weren't just positive reviews – they were evidence that we had built something that materially improved how businesses operated on a daily basis.

Giving SMEs their time back

Open banking & payment splitting meant SMEs got paid more quickly and regularly

Smart cashflow management with a full view of all company finances present and future

The Breakthrough

The moments that made it feel possible

Giving SMEs their time back

Open banking & payment splitting meant SMEs got paid more quickly and regularly

Smart cashflow management with a full view of all company finances present and future

Investment validation arrived in the form of £1.6 million from Lakestar and Six Fintech – venture capital firms that understood both the fintech landscape and the specific pain points plaguing SMEs. These weren't just cheques; they were stamps of approval from investors who had seen countless payment solutions fail to gain traction. Their backing suggested that our approach to the problem was fundamentally sound, even if the execution remained to be proven.

The regulatory milestone came faster than anyone predicted. Achieving FCA authorisation for Account Information Services and Payment Initiation Services in just three months demonstrated that our compliance approach was robust and our team understood the complexities of financial regulation. While other startups struggled with regulatory hurdles for years, we had built the right foundations from the beginning. The authorisation wasn't just a legal requirement – it was proof that we could operate at the standards required to handle other people's money.

"The first time a customer told us they'd cancelled their debt collection service because they didn't need it anymore, we knew we'd found something real."

First customer wins validated every assumption about product-market fit. Businesses immediately embraced features that seemed obvious in hindsight but had never been available before. Payment URLs that could be copied and sent via email, WhatsApp, or any communication channel eliminated the friction of platform lock-in. Real-time cash flow dashboards gave business owners what Tom Whittle called "brilliant" visibility into their financial position. The automation meant companies could focus on serving customers instead of chasing payments.

The technology proved itself under real-world conditions that no amount of testing could replicate. Successfully integrating with all major UK banks despite the early instability of open banking infrastructure required constant troubleshooting and adaptation. When payment requests consistently completed successfully and money arrived in business accounts as promised, the platform demonstrated the reliability that cash-strapped SMEs desperately needed. Technical excellence became the foundation for customer trust.

Market feedback confirmed that we had identified something genuinely transformative. Customers consistently described Juno as "cheaper and faster than other payment alternatives we've used like GoCardless or PayPal." Amanda Baker noted that "every penny counts for small business owners like me." The testimonials weren't just positive reviews – they were evidence that we had built something that materially improved how businesses operated on a daily basis.

Innovation Execution

Building a platform that SMEs actually wanted

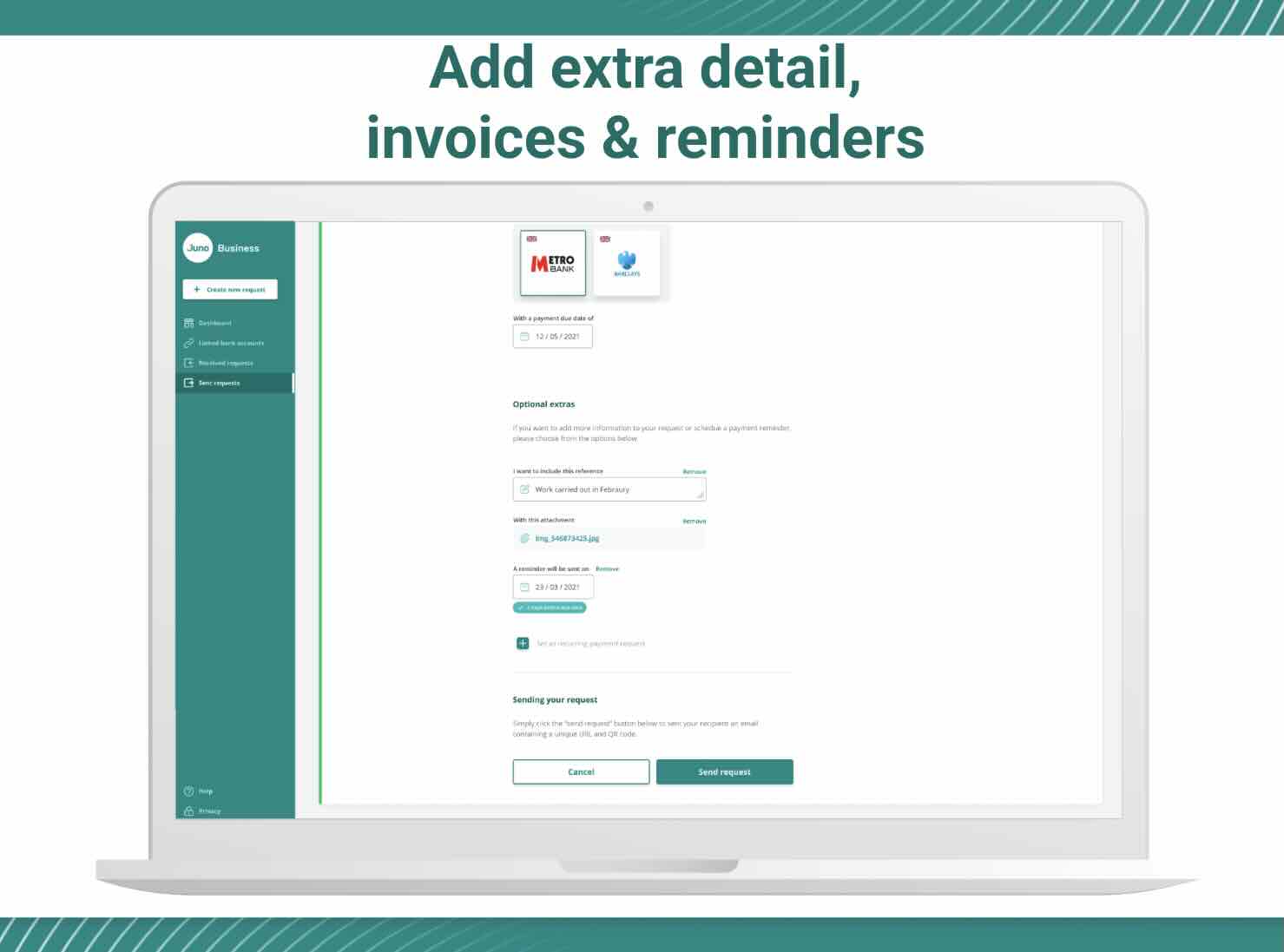

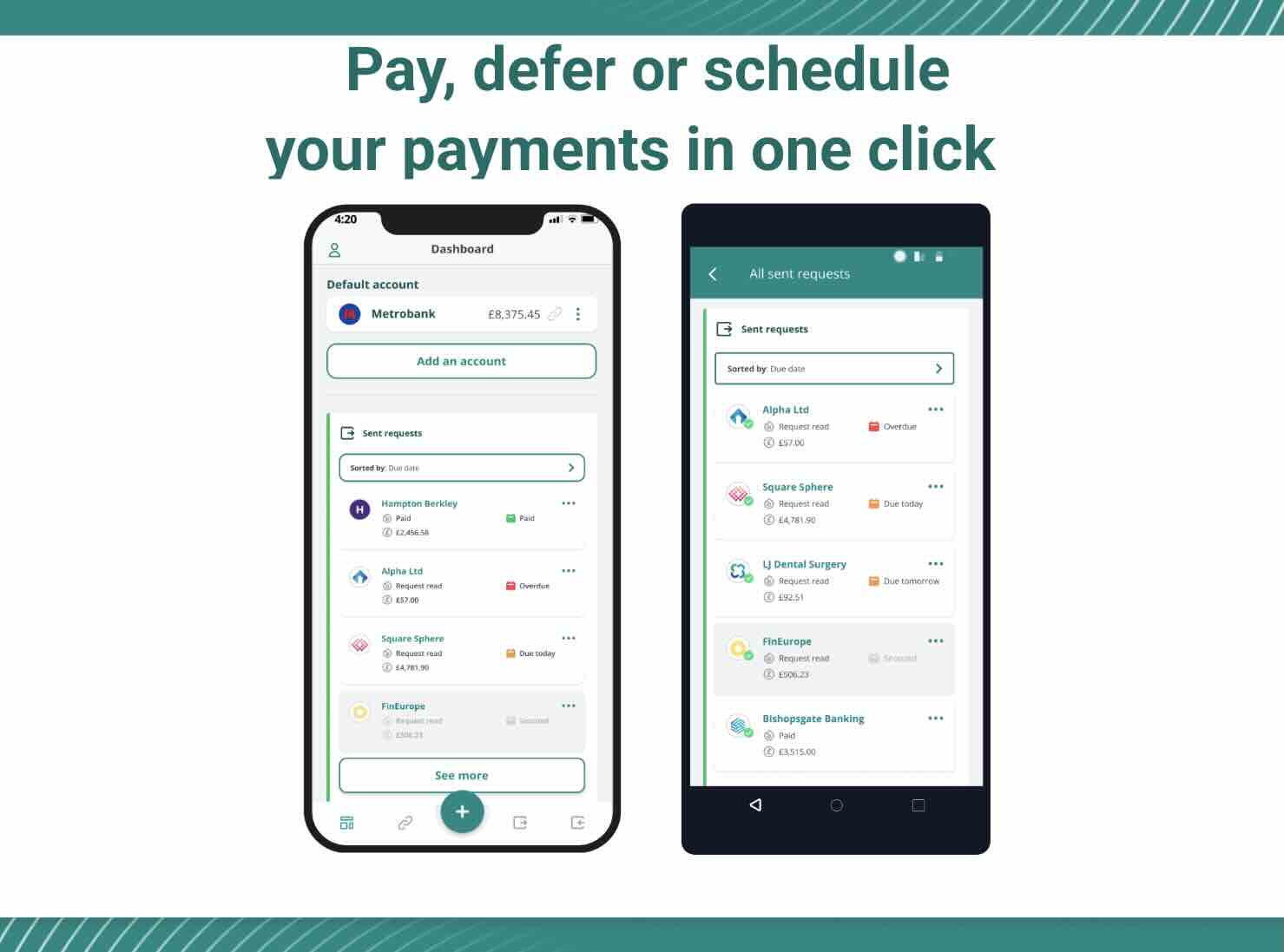

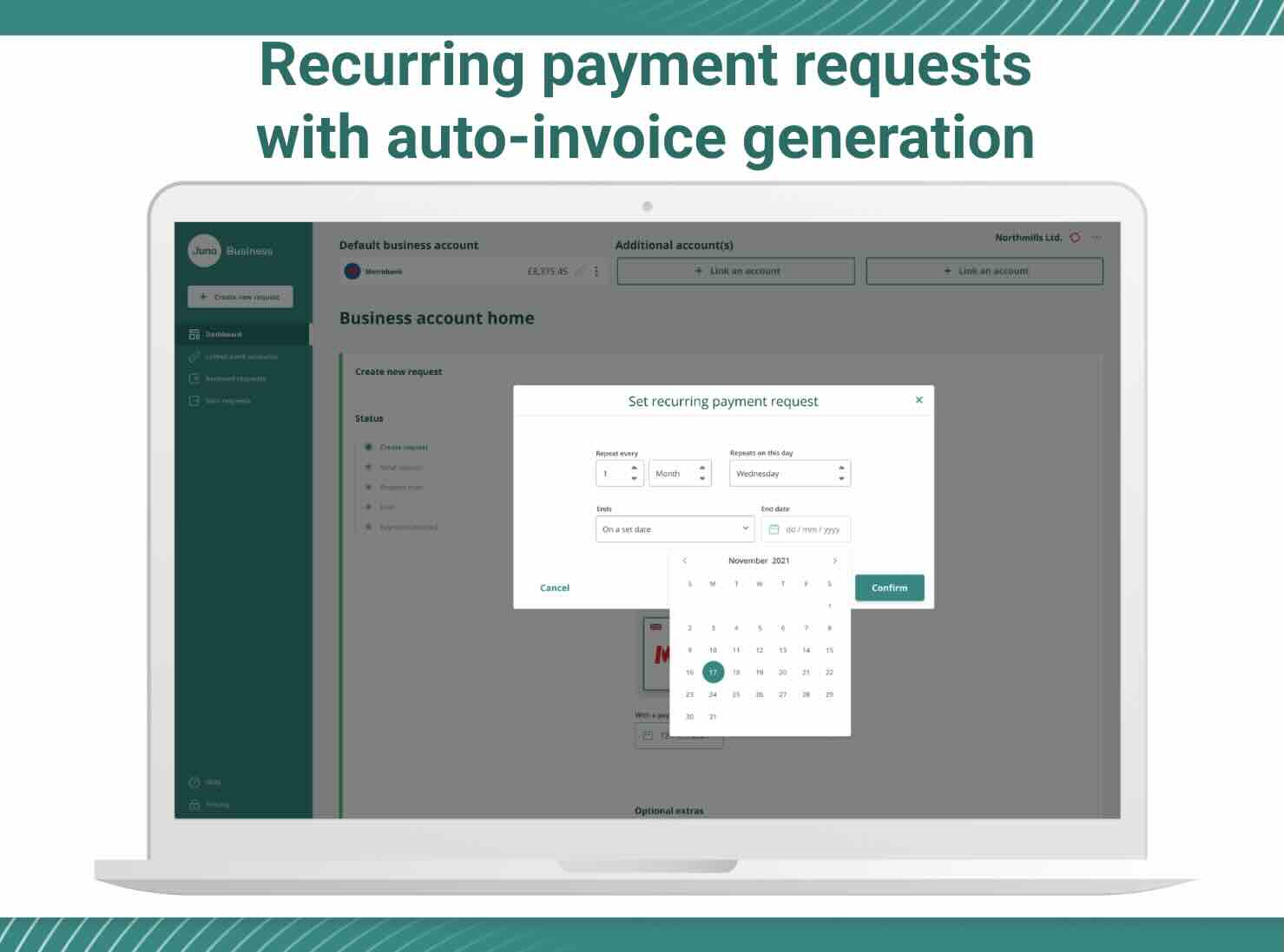

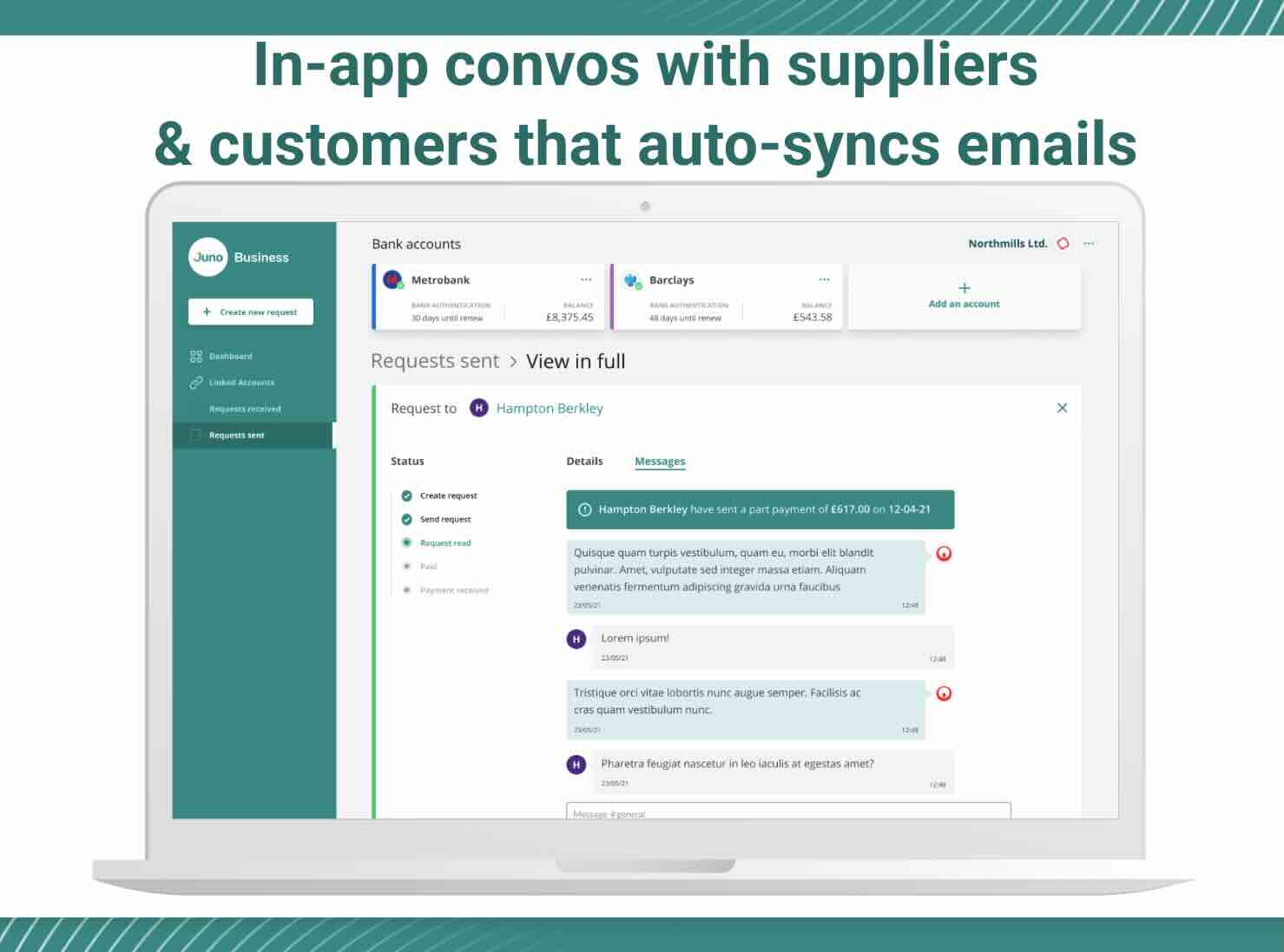

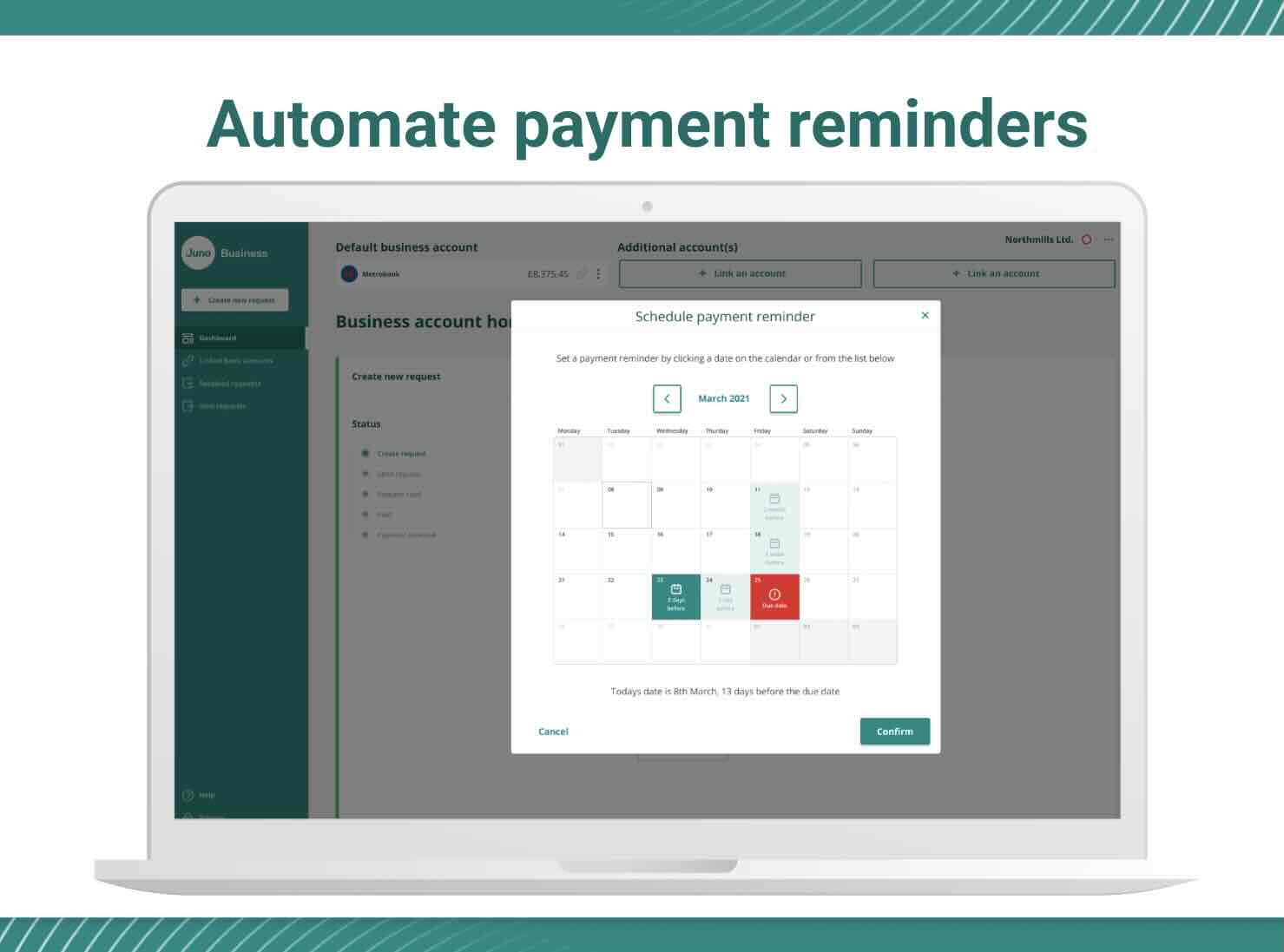

Payment flexibility emerged as the killer feature that separated Juno from every existing solution. The ability to schedule payments (& reminders) gave businesses control over cash flow timing that traditional invoicing could never provide. Part payments acknowledged the reality that customers sometimes needed to pay in instalments, while 'snooze' functionality recognised that temporary payment delays were often better than permanent customer loss. These were acknowledgements of how business relationships actually worked in practice.

The distribution breakthrough came through copyable payment URLs that liberated businesses from platform constraints. Instead of forcing customers through specific payment flows or proprietary interfaces, businesses could generate a unique URL and send it anywhere – email, WhatsApp, SMS, even printed on invoices. This simple innovation removed friction from the payment process while giving businesses complete control over how they communicated with customers. The technology enabled the relationship; it didn't dictate it.

"Innovation isn't just about new technology. It's about rethinking ways of working that no-one believed could be simplified.""

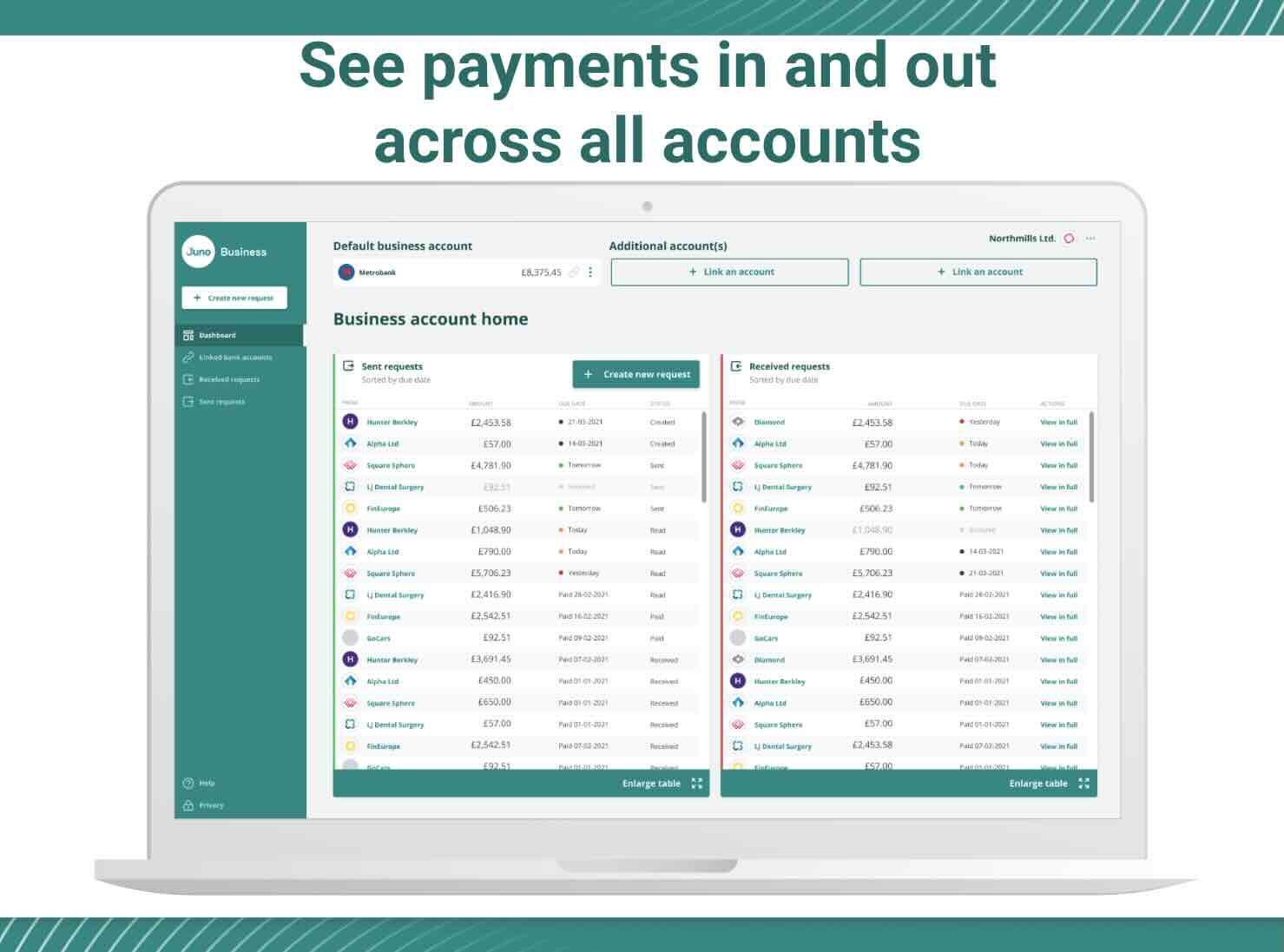

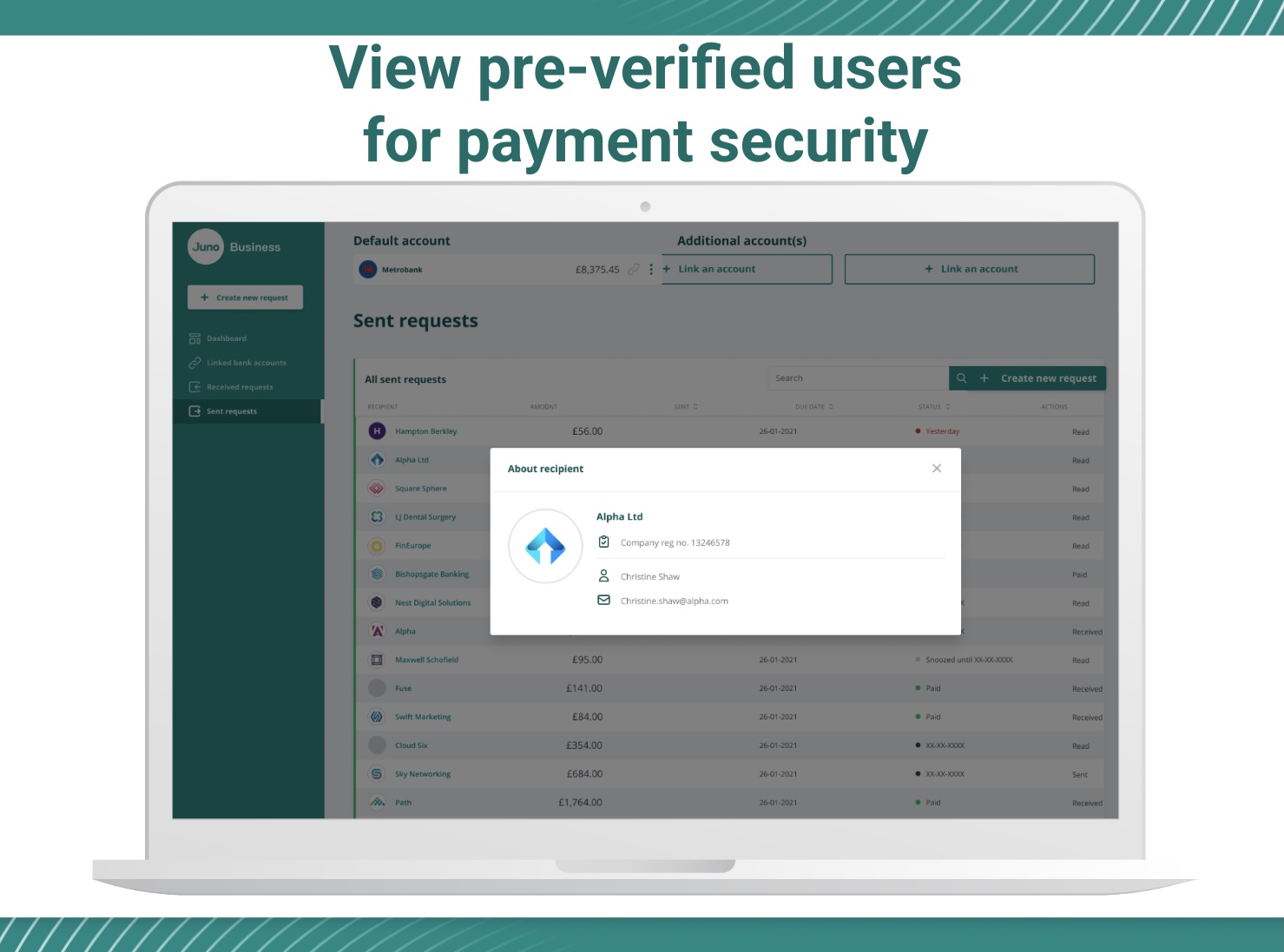

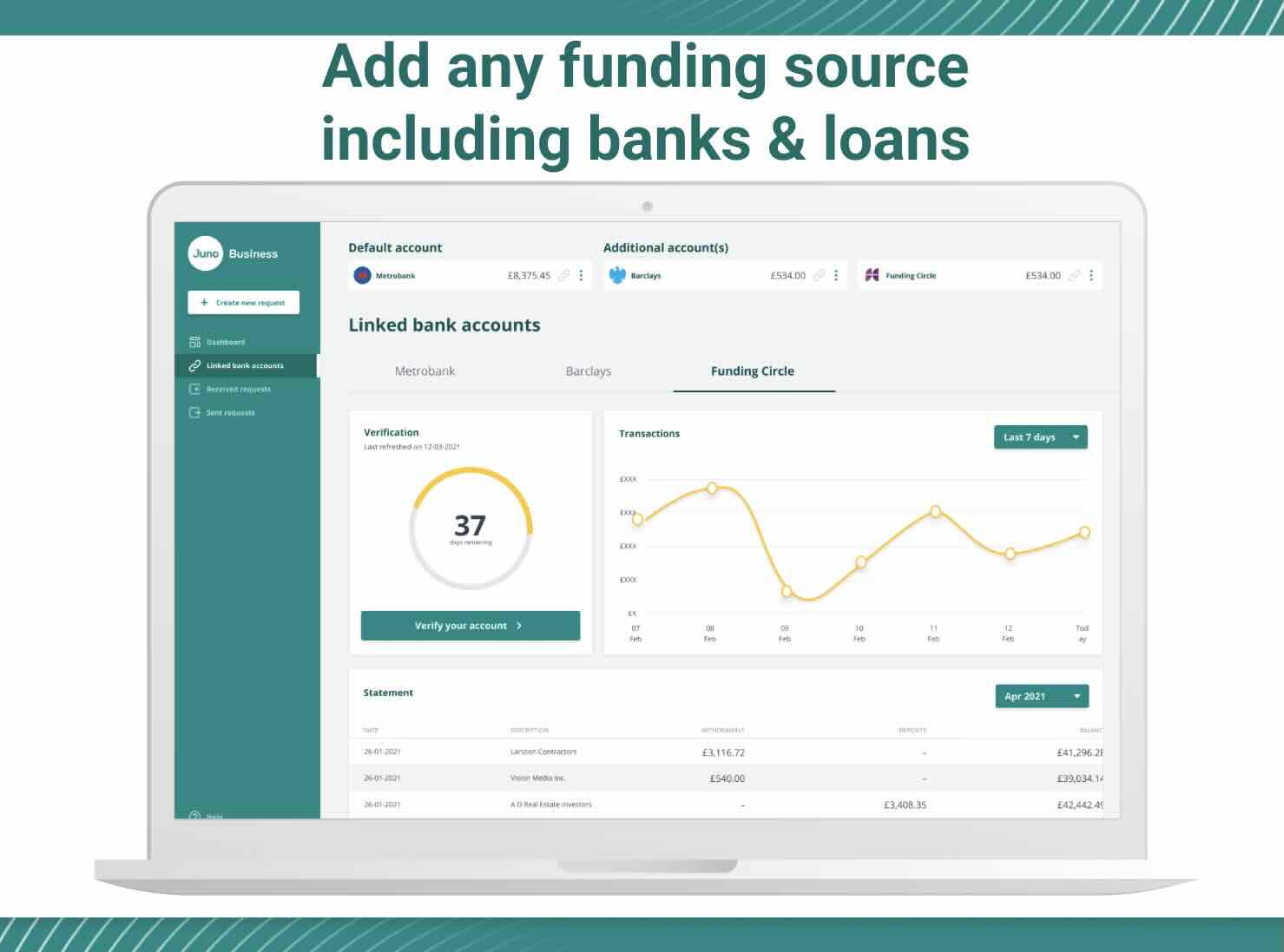

Financial visibility tools addressed the fundamental cash flow blindness that plagued SMEs across every sector. Multi-bank account linking provided a unified view across all business finance sources, eliminating the need to log into multiple banking platforms just to understand current financial position. Mobile-first cash flow management meant business owners could check their position, approve payments, and make critical decisions from anywhere. The goal was to transform financial management from a time-consuming chore into effortless situational awareness.

Ecosystem expansion validated the platform approach through debt recovery and Buy Now, Pay Later products that increased revenue per customer by 82% in just six months. Rather than building a single-purpose payment tool, we had created infrastructure that could support multiple financial services. Customers who came for simple payment processing stayed for comprehensive cash flow management. The 82% revenue increase demonstrated that when you solve the core problem properly, additional services become natural extensions rather than forced upsells.

Customer experience improvements focused relentlessly on removing administrative burden from business operations. Automatic reminders meant no more manual follow-up emails. Real-time payment tracking provided instant status updates without requiring customers to log into separate systems. Refund capabilities simplified the resolution of disputes or returns. Every feature was designed to answer two simple question: how can we give business owners their time back and how can we simplify the invoice payments for the payer?

Visual documentation from the innovation execution phase

Visual documentation from the innovation execution phase

Visual documentation from the innovation execution phase

Innovation Execution

Building a platform that SMEs actually wanted

Visual documentation from the innovation execution phase

Visual documentation from the innovation execution phase

Visual documentation from the innovation execution phase

Payment flexibility emerged as the killer feature that separated Juno from every existing solution. The ability to schedule payments (& reminders) gave businesses control over cash flow timing that traditional invoicing could never provide. Part payments acknowledged the reality that customers sometimes needed to pay in instalments, while 'snooze' functionality recognised that temporary payment delays were often better than permanent customer loss. These were acknowledgements of how business relationships actually worked in practice.

The distribution breakthrough came through copyable payment URLs that liberated businesses from platform constraints. Instead of forcing customers through specific payment flows or proprietary interfaces, businesses could generate a unique URL and send it anywhere – email, WhatsApp, SMS, even printed on invoices. This simple innovation removed friction from the payment process while giving businesses complete control over how they communicated with customers. The technology enabled the relationship; it didn't dictate it.

"Innovation isn't just about new technology. It's about rethinking ways of working that no-one believed could be simplified.""

Financial visibility tools addressed the fundamental cash flow blindness that plagued SMEs across every sector. Multi-bank account linking provided a unified view across all business finance sources, eliminating the need to log into multiple banking platforms just to understand current financial position. Mobile-first cash flow management meant business owners could check their position, approve payments, and make critical decisions from anywhere. The goal was to transform financial management from a time-consuming chore into effortless situational awareness.

Ecosystem expansion validated the platform approach through debt recovery and Buy Now, Pay Later products that increased revenue per customer by 82% in just six months. Rather than building a single-purpose payment tool, we had created infrastructure that could support multiple financial services. Customers who came for simple payment processing stayed for comprehensive cash flow management. The 82% revenue increase demonstrated that when you solve the core problem properly, additional services become natural extensions rather than forced upsells.

Customer experience improvements focused relentlessly on removing administrative burden from business operations. Automatic reminders meant no more manual follow-up emails. Real-time payment tracking provided instant status updates without requiring customers to log into separate systems. Refund capabilities simplified the resolution of disputes or returns. Every feature was designed to answer two simple question: how can we give business owners their time back and how can we simplify the invoice payments for the payer?

Scaling & Growth

From proof of concept to real business

Team building became the foundation for everything that followed. Recruiting talent from Zopa brought deep fintech expertise and regulatory knowledge. Hiring from Nutmeg added investment platform experience and customer operations capability. Bringing in people from Huckletree contributed community building and startup ecosystem understanding. Each hire was chosen not just for their technical skills, but for their experience building financial services that real businesses depended on daily.

Customer traction demonstrated genuine product-market fit across diverse industry sectors. Reaching 5000+ SME customers within 6 months proved that the pain point was universal and our solution was compelling. These weren't just trial users or free accounts – they were businesses integrating Juno into their core operations and depending on our platform for critical cash flow management. Customer retention and engagement metrics showed that once businesses experienced the difference, they didn't want to go back to manual payment chasing.

"Growth in fintech isn't just about user numbers. It's about proving you can handle other people's money responsibly at scale."

Strategic partnerships expanded reach and credibility across the business ecosystem. Developing relationships with 10 technology partners created integration opportunities that made Juno more valuable to existing customers while opening new distribution channels. Connections with tier-1 corporates like Barclays and established organisations like the Federation of Small Businesses provided credibility that helped smaller businesses trust a young fintech with their payment processing. Each partnership was chosen for strategic value, not just prestige.

Product success metrics validated the platform approach through features that genuinely improved business outcomes. The debt recovery and BNPL products were solutions to real problems that emerged from customer conversations. When customers like Tom Whittle of Mission described the dashboard as giving them "a picture of your business' finances while Juno chases outstanding payments for you," it confirmed that we had built something that resonated with SMEs.

Infrastructure scaling prepared the platform for the growth that everyone expected would follow. Building systems capable of handling increasing transaction volumes, maintaining regulatory compliance as operations expanded, and managing customer support for a growing user base required investment in operational excellence that wasn't visible to customers but was critical for long-term success. The goal was to create a foundation that could support the next phase of growth without compromising on reliability or security.

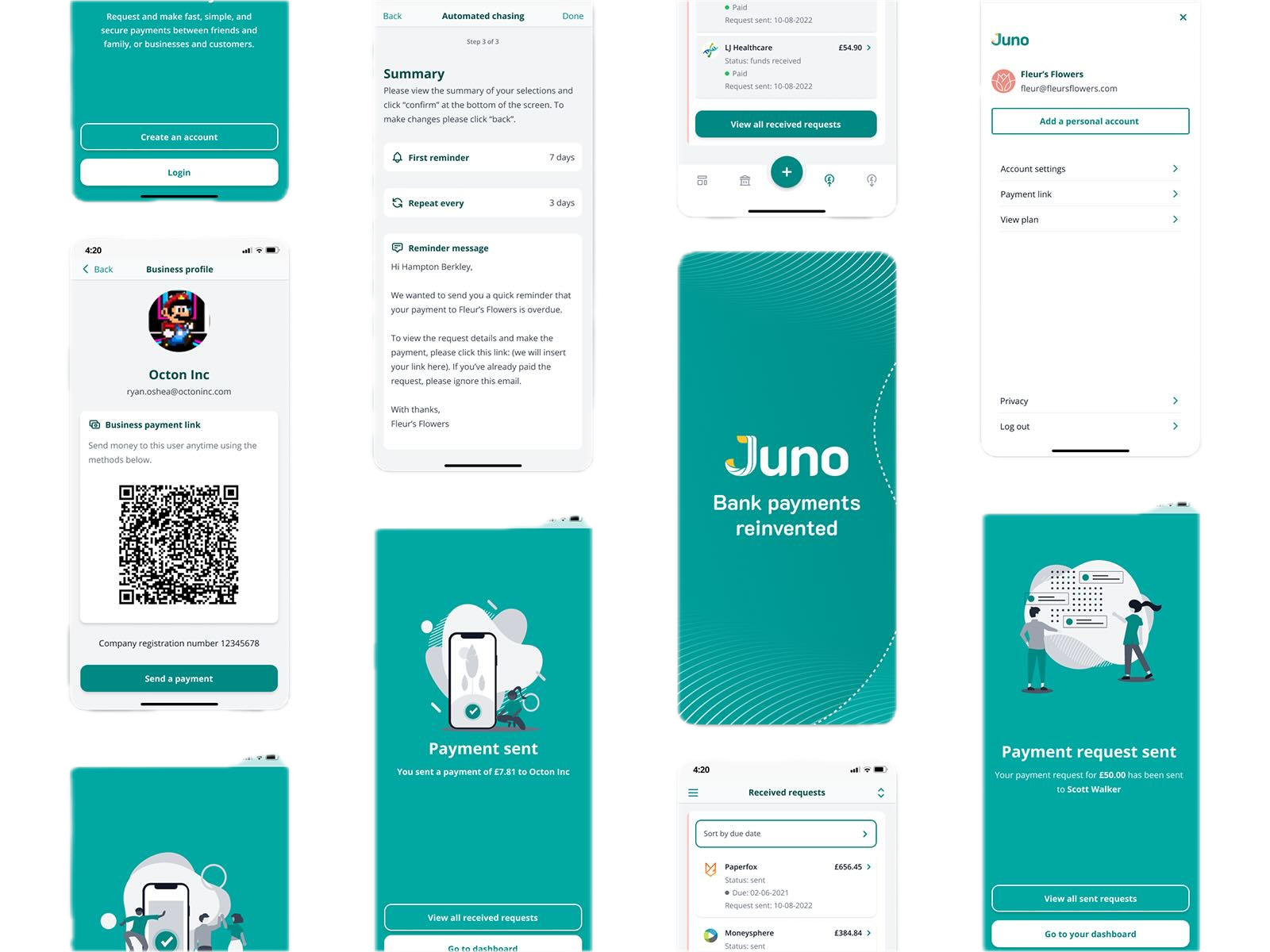

Visual documentation from the scaling & growth phase

Visual documentation from the scaling & growth phase

Visual documentation from the scaling & growth phase

Scaling & Growth

From proof of concept to real business

Visual documentation from the scaling & growth phase

Visual documentation from the scaling & growth phase

Visual documentation from the scaling & growth phase

Team building became the foundation for everything that followed. Recruiting talent from Zopa brought deep fintech expertise and regulatory knowledge. Hiring from Nutmeg added investment platform experience and customer operations capability. Bringing in people from Huckletree contributed community building and startup ecosystem understanding. Each hire was chosen not just for their technical skills, but for their experience building financial services that real businesses depended on daily.

Customer traction demonstrated genuine product-market fit across diverse industry sectors. Reaching 5000+ SME customers within 6 months proved that the pain point was universal and our solution was compelling. These weren't just trial users or free accounts – they were businesses integrating Juno into their core operations and depending on our platform for critical cash flow management. Customer retention and engagement metrics showed that once businesses experienced the difference, they didn't want to go back to manual payment chasing.

"Growth in fintech isn't just about user numbers. It's about proving you can handle other people's money responsibly at scale."

Strategic partnerships expanded reach and credibility across the business ecosystem. Developing relationships with 10 technology partners created integration opportunities that made Juno more valuable to existing customers while opening new distribution channels. Connections with tier-1 corporates like Barclays and established organisations like the Federation of Small Businesses provided credibility that helped smaller businesses trust a young fintech with their payment processing. Each partnership was chosen for strategic value, not just prestige.

Product success metrics validated the platform approach through features that genuinely improved business outcomes. The debt recovery and BNPL products were solutions to real problems that emerged from customer conversations. When customers like Tom Whittle of Mission described the dashboard as giving them "a picture of your business' finances while Juno chases outstanding payments for you," it confirmed that we had built something that resonated with SMEs.

Infrastructure scaling prepared the platform for the growth that everyone expected would follow. Building systems capable of handling increasing transaction volumes, maintaining regulatory compliance as operations expanded, and managing customer support for a growing user base required investment in operational excellence that wasn't visible to customers but was critical for long-term success. The goal was to create a foundation that could support the next phase of growth without compromising on reliability or security.

The Legacy

Ideas bigger than their first implementation

The technology foundation outlived the company that created it. When we were forced to close Juno, the intellectual property and integrations were acquired by other companies that recognised the value of what had been built. The open banking infrastructure, payment automation systems, and customer management tools continued solving payments problems under different ownership. Technical innovations that took months to develop found new life in products that carried the mission forward, proving that good ideas transcend their original implementations.

Market education impact extended far beyond our customer base. By demonstrating that business payments could work differently, Juno contributed to broader open banking understanding across the SME sector. Competitors and new entrants adopted similar approaches to user experience and automation. Industry events and publications regularly referenced our innovations as examples of what was possible when fintech focused on real business problems rather than flashy features. The education rippled outward, raising expectations for what payment solutions should deliver.

"The hardest part about startup failure isn't losing the company. It's knowing the problem you were solving is still out there, still hurting people."

Customer transformations created lasting change in how businesses approached cash flow management. Companies that experienced automated payment tracking, real-time financial visibility, and effortless payment collection often continued using similar practices even after moving to different platforms. The behaviours and expectations that Juno enabled (expecting instant settlement, demanding payment automation, requiring multi-channel distribution) became standard operating procedures that improved business efficiency regardless of the underlying technology. A few years down the line, Mimo, with whom I was a board advisor, took our vision at Juno to a whole new level by integrating credit to solve the final underlying problem we hadn't.

Industry influence established user experience patterns that became standard practice for B2B payments. The copyable payment URL, multi-bank account linking, and mobile-first cash flow management became features that customers expected from any modern payment solution. Product managers at competing platforms regularly referenced Juno's approach to automation and customer experience. What began as innovative features became table stakes for credible business payment solutions.

Regulatory contributions emerged from being part of the early adopter group that helped shape how open banking evolved for business use cases. Our experience with FCA authorisation, bank API integrations, and customer protection requirements provided valuable feedback to regulators and industry bodies about what worked and what needed improvement. The compliance frameworks and security practices we developed influenced standards and best practices that benefited the entire open banking ecosystem.

Visual documentation from the the legacy phase

Visual documentation from the the legacy phase

Visual documentation from the the legacy phase

The Legacy

Ideas bigger than their first implementation

Visual documentation from the the legacy phase

Visual documentation from the the legacy phase

Visual documentation from the the legacy phase

The technology foundation outlived the company that created it. When we were forced to close Juno, the intellectual property and integrations were acquired by other companies that recognised the value of what had been built. The open banking infrastructure, payment automation systems, and customer management tools continued solving payments problems under different ownership. Technical innovations that took months to develop found new life in products that carried the mission forward, proving that good ideas transcend their original implementations.

Market education impact extended far beyond our customer base. By demonstrating that business payments could work differently, Juno contributed to broader open banking understanding across the SME sector. Competitors and new entrants adopted similar approaches to user experience and automation. Industry events and publications regularly referenced our innovations as examples of what was possible when fintech focused on real business problems rather than flashy features. The education rippled outward, raising expectations for what payment solutions should deliver.

"The hardest part about startup failure isn't losing the company. It's knowing the problem you were solving is still out there, still hurting people."

Customer transformations created lasting change in how businesses approached cash flow management. Companies that experienced automated payment tracking, real-time financial visibility, and effortless payment collection often continued using similar practices even after moving to different platforms. The behaviours and expectations that Juno enabled (expecting instant settlement, demanding payment automation, requiring multi-channel distribution) became standard operating procedures that improved business efficiency regardless of the underlying technology. A few years down the line, Mimo, with whom I was a board advisor, took our vision at Juno to a whole new level by integrating credit to solve the final underlying problem we hadn't.

Industry influence established user experience patterns that became standard practice for B2B payments. The copyable payment URL, multi-bank account linking, and mobile-first cash flow management became features that customers expected from any modern payment solution. Product managers at competing platforms regularly referenced Juno's approach to automation and customer experience. What began as innovative features became table stakes for credible business payment solutions.

Regulatory contributions emerged from being part of the early adopter group that helped shape how open banking evolved for business use cases. Our experience with FCA authorisation, bank API integrations, and customer protection requirements provided valuable feedback to regulators and industry bodies about what worked and what needed improvement. The compliance frameworks and security practices we developed influenced standards and best practices that benefited the entire open banking ecosystem.

What This Taught Me

A premature end to a whirlwind journey

Partnership dependency risk became painfully clear when Darren's promised transition to CEO collapsed at the worst possible moment. He had committed to joining as CEO, which our second VC funding tranche was contingent upon, and we had budgeted every penny based on that certainty. When he revealed he'd decided to stay at Crowdcube, leaving us with just 30 days of runway instead of the expected £800,000, the lesson was immediate, brutal and fatal. This became the company's premature death sentence when our growth and metrics looked promising.

Technical integration realities proved far more complex than vendor promises suggested. Yapily's "plug and play" open banking integration required constant bank API troubleshooting, with major institutions dragging their heels on compliance requirements that were supposedly mandatory. What should have been seamless connectivity became a daily firefighting exercise as banks implemented open banking standards inconsistently and support systems remained inadequate. Early adopters pay the price for immature infrastructure, regardless of regulatory requirements.

"The most expensive lesson was learning that promises from advisors and partners need the same due diligence as everything else. One person's word became a company's death sentence."

Market timing challenges emerged from being early in open banking adoption when education was as important as execution. Customers needed to understand not just why Juno was better than existing solutions, but why open banking payments were safe, reliable, and legally protected. Regulatory bodies like the Open Banking Implementation Entity provided insufficient support for early innovators, focusing on compliance over adoption. Being right about the future technology direction doesn't guarantee market readiness for that future.

Customer behaviour inertia proved stronger than expected, even when new solutions offered clear advantages. Shifting established B2B payment habits required not just better features, but sustained education about why change was worth the effort. Businesses that complained about late payments and manual processes still hesitated to adopt automated alternatives because they felt that the payer wouldn't use them. They were right, and Mimo solved this years later by integrating credit. The gap between recognising a problem and embracing a solution can persist long after viable options become available.

Capital efficiency in regulated markets demanded different planning approaches than typical software startups. FCA authorisation and ongoing compliance consumed resources faster than anticipated, requiring legal expertise, security infrastructure, and operational overhead that didn't directly drive customer acquisition. The regulatory foundation necessary for financial services creates fixed costs that must be factored into growth models from day one. Underestimating compliance overhead is a luxury that fintech startups cannot afford.

Visual documentation from the what this taught me phase

Visual documentation from the what this taught me phase

Visual documentation from the what this taught me phase

What This Taught Me

A premature end to a whirlwind journey

Visual documentation from the what this taught me phase

Visual documentation from the what this taught me phase

Visual documentation from the what this taught me phase

Partnership dependency risk became painfully clear when Darren's promised transition to CEO collapsed at the worst possible moment. He had committed to joining as CEO, which our second VC funding tranche was contingent upon, and we had budgeted every penny based on that certainty. When he revealed he'd decided to stay at Crowdcube, leaving us with just 30 days of runway instead of the expected £800,000, the lesson was immediate, brutal and fatal. This became the company's premature death sentence when our growth and metrics looked promising.

Technical integration realities proved far more complex than vendor promises suggested. Yapily's "plug and play" open banking integration required constant bank API troubleshooting, with major institutions dragging their heels on compliance requirements that were supposedly mandatory. What should have been seamless connectivity became a daily firefighting exercise as banks implemented open banking standards inconsistently and support systems remained inadequate. Early adopters pay the price for immature infrastructure, regardless of regulatory requirements.

"The most expensive lesson was learning that promises from advisors and partners need the same due diligence as everything else. One person's word became a company's death sentence."

Market timing challenges emerged from being early in open banking adoption when education was as important as execution. Customers needed to understand not just why Juno was better than existing solutions, but why open banking payments were safe, reliable, and legally protected. Regulatory bodies like the Open Banking Implementation Entity provided insufficient support for early innovators, focusing on compliance over adoption. Being right about the future technology direction doesn't guarantee market readiness for that future.

Customer behaviour inertia proved stronger than expected, even when new solutions offered clear advantages. Shifting established B2B payment habits required not just better features, but sustained education about why change was worth the effort. Businesses that complained about late payments and manual processes still hesitated to adopt automated alternatives because they felt that the payer wouldn't use them. They were right, and Mimo solved this years later by integrating credit. The gap between recognising a problem and embracing a solution can persist long after viable options become available.

Capital efficiency in regulated markets demanded different planning approaches than typical software startups. FCA authorisation and ongoing compliance consumed resources faster than anticipated, requiring legal expertise, security infrastructure, and operational overhead that didn't directly drive customer acquisition. The regulatory foundation necessary for financial services creates fixed costs that must be factored into growth models from day one. Underestimating compliance overhead is a luxury that fintech startups cannot afford.

"The future of business intelligence is not about having more data—it is about having better insights that drive immediate action."

Key Impact Metrics

Quantifying the transformation and lasting impact across multiple dimensions.

SME Customers

SME customers onboarded across diverse UK business sectors

Investment Raised

Strategic investment from Lakestar & Six Fintech (UBS/Credit Suisse)

Revenue Increase

Increase in revenue per customer through debt recovery and BNPL products

Strategic Partnerships

Strategic partnerships with tech and finance companies like Barclays

Months

FCA authorisation secured in 3 months for AIS and PIS

Banks Integrated

Separate banking integrations connected to Juno

MoM Customer Growth

Month on month customer growth over 6 months

Weekly Active Users

Percentage of customers that made and requested payments weekly

Month Payback Period

Number of months to payback acquisition investment

Alliance Block

"All SMEs worry about being paid late and managing their cash flow. Juno arms small businesses with a real-time view of payments so they can forecast accurately and gets you paid more quickly without the hassle."

Amber Ghaddar

Founder

Mission

"The dashboard is brilliant. It shows business cash flow in real-time, so you can get a picture of your business' finances while Juno chases outstanding payments for you."

Tom Whittle

Founder & CEO

5 Stories

"Juno is cheaper and faster than other payment alternatives we've used like GoCardless or PayPal. Every penny counts for startup owners like me."

Amanda Baker

Founder & Story Strategist

Coffeeworks

"A way of having fewer sleepless nights"

John Saunders

Managing Director

Peninsula Hearing Care

"Closer to real-time and it actually works for you not against you. Way better than the half-way picture from Xero."

Laurie McKenna

Managing Director

Matt Brinton Coaching

"A much more fully featured version of challenger bank web interfaces and we're already seeing invoices being paid weeks earlier."

Matt Brinton

Founder & Coach

Behind the Scenes

A glimpse into our journey